Here we are yet again. With the calendar flipping to December, 2022 is almost at an end. This year was not like many we have had in recent years, in fact, it was essentially a counter trend to everything we have seen in the last decade. Macroeconomic conditions fundamentally changed throughout 2022. Inflation roared back in the post-covid induced monetary stimulus world, and central banks around the world were forced to tighten significantly by hiking interest rates at a speed we have never seen. Global currencies depreciated significantly as the flight to quality in the U.S. dollar ensued. Oil staged a major comeback as economic conditions were supercharged in early 2022, although some gains have been given back recently. Global recession fears are at their highest level since the Great Financial Crisis, all but ensuring that we see one in most major developed and undeveloped countries by next year. Even safety plays like fixed income were battered as interest rates rose, failing the traditional 60/40 portfolios as we know them.

In an environment like this, one thing rang true, and it has been a while since we've been able to really champion it. Active management has been a significant contributor to outperformance, beating passive investors significantly. Although many investors have run to the passive strategy of 'buying an index’, 2022 proved that this approach is not a good one during uncertain times. It's an acceptable strategy when things are going well, and markets are rising, but when choppy markets come, you want to be nimble, confident, and make smart decisions in real-time.

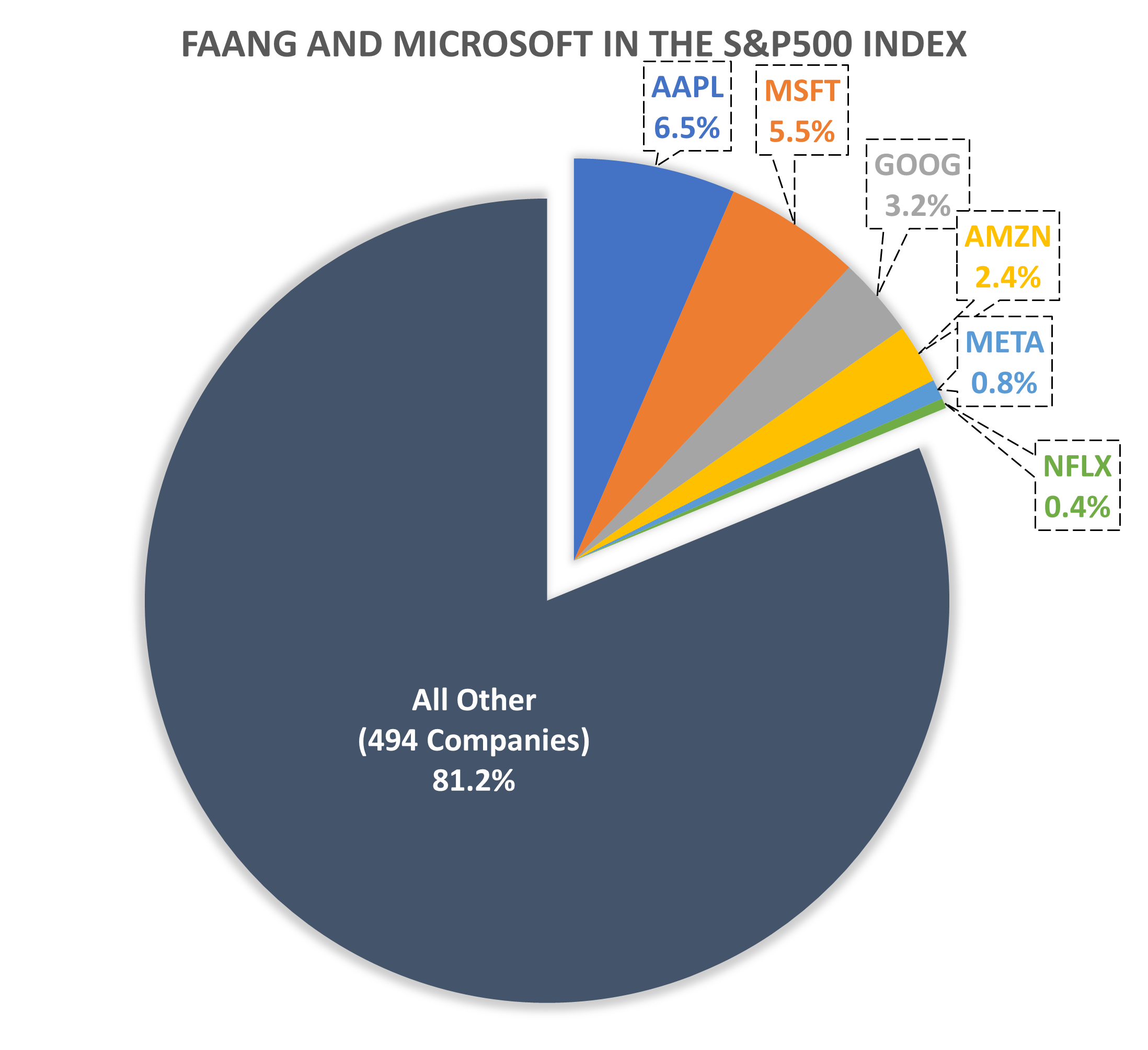

With the growth of Exchange Traded Funds in the last decade, we have seen a similar increase in the prevalence of passive investing. And it is true that passive investing has had an impressive run in beating active managers. However, that claim comes with a few caveats. One is that the outperformance of passive investing in vehicles such as the S&P 500 Index can be attributed to just a handful of companies, and those few companies have grown to a significant proportion of these passive holdings. Just take a look at the graphic: FAANG and Microsoft in the S&P 500 Index.

The S&P 500 Index has been led by these megacap tech companies, which make up a significant portion of the overall index, almost 20% of the entire holding. At the time of posting, the weight of Apple (6.5%), and Microsoft (5.5%), were higher than the entire sectors of Utilities (3.2%) Real Estate (3.1%) and Materials (2.5%) combined! When highly-weighted individual companies do well, and those correlated holdings do well, it is increasingly difficult for active managers to outperform without exposure to the same companies – and then you're really only index hugging.

What changed in 2022? A few things were mentioned above - interest rates increased, and monetary stimulus turned into tightening, making it increasingly difficult for these tech giants to grow their bottom lines and less likely the market would pay up for future growth that was less valuable than in the days of super low interest rates. Inflation, too, had an effect, as returns from 'real' tangible assets ripped higher this year. The commonality was that these leaders turned into laggards – and so did passive investing. Utilizing active investing, you are able to choose your portfolio’s exposure to defensive vs. aggressive issues. You can trim holdings as their dollar weighting increases and shift allocations to underperforming sectors as economic conditions change. You can move from growth assets during an expansionary macroeconomic background to value assets during recessionary periods. And that's exactly what Goodreid has done throughout 2022.

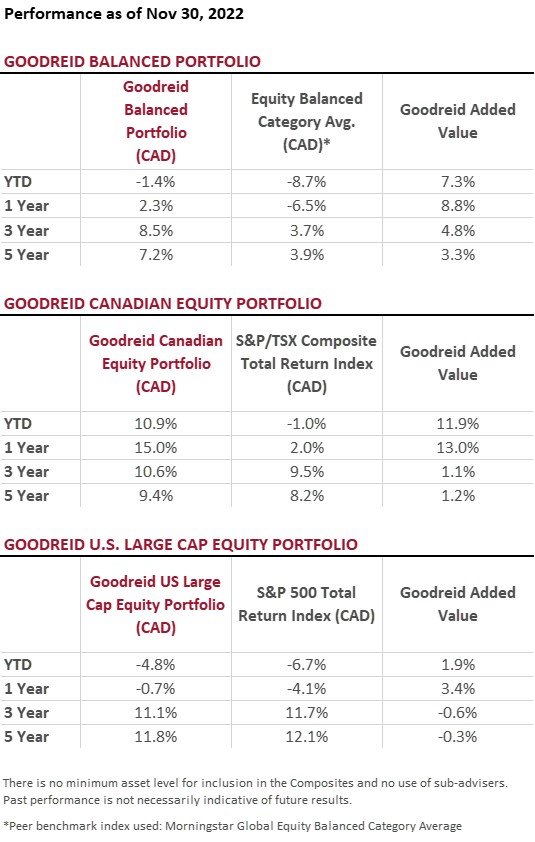

Goodreid held certain assets in 2022 that did well, while others fell behind. The most significant outperformer this year was our Canadian equity portfolio. Within this portfolio, we moved our oil and gas weighting to equal weight vs. the index in February, as we became aware that the 'transitory' inflation being experienced would become more entrenched than temporary. We also forecasted that the supply and demand imbalance would persist for a significant amount of time, and with the addition of Russia's war in Ukraine, there would likely be outperformance in oil and gas assets. By April it was evident that equity markets were entrenched in a bear market, leading us to increase the quality of the holdings within our portfolio, expand the number of holdings, and increase our dividend yield. As can be seen in the table, active decisions have led to a double-digit outperformance this year, which we are proud to have accomplished for our clients.

We also made significant moves in our U.S. portfolios to protect capital and help grow our clients’ wealth. In Q2, we sold the balance of our META (formerly Facebook) holdings after selling the first tranche in mid 2021, a move that has proven financially worthwhile. Our average selling price of $240/share is more than double its current quotation. We were proactive with Apple, trimming 35% of our holdings at $169/share, and Lowes, trimming at $211/share, containing risk by “right-sizing” these issues. Long-term investing coupled with opportunistic harvesting of gains when appropriate has been a winning formula. We're seeing the results across Goodreid’s portfolios.

While we are pleased with our outperformance of the markets, we are also particularly happy with how Goodreid’s Balanced Portfolio Composite stacks up against other investment managers in Canada. When compared to a third-party composite with a similar investment focus, the Morningstar Global Equity Balanced Category Average, which includes over 1000 Canadian fund managers of Balanced funds with global exposure, Goodreid’s portfolio ranks in the 96th to 99th percentile in the last 5 years, depending on the timeframe.

Back