Investment lore tells us that “there’s gold in them there hills”, when it comes to initial public offerings (IPOs) of stocks. Surely everyone has heard stories of those fortunate enough to “get in on the ground floor” of McDonalds, Microsoft, Tim Hortons, Apple, Dollarama, Amazon, etc. and the countless number of times those stocks have multiplied since then. Faced with tales of eye-popping returns like these, it’s tempting to conclude that initial public offerings are a great investment opportunity. Reality however is different, and accordingly, our practice is to cast a wary and cautious eye towards all IPOs. Why?

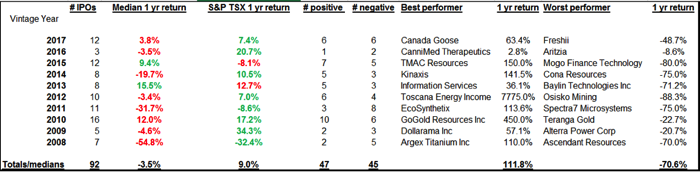

The best way to answer this question is to jump directly to the conclusion: the typical IPO stock, not only doesn’t multiply 10-fold like some of the market darlings above, but in fact doesn’t even keep pace with the S&P 500 Index. Over the last decade, the Bloomberg IPO Index, which tracks the performance of U.S. IPOs in their first year, has generated a total return of just 59% whereas the S&P 500 has returned 105%. In Canada, among the 92 initial public offerings on the TSX over the last ten years, just 47 made gains in their first year. The typical IPO underperformed the S&P TSX Composite Index with remarkable consistency, lagging the index in eight of the last ten years, such that the typical IPO buyer incurred a loss of 3.5% per year, whereas the TSX earned 9% in a typical year. The monetary incentives in place for sellers and their agents to inflate IPO prices, the risk of the seller being better informed about a company’s prospects than the buyer, the need for management to demonstrate credibility in setting performance targets and the risk of adverse selection, sometimes known as “the winner’s curse” all contribute to this dramatic and consistent underperformance of initial public offerings in their rookie year.

When evaluating an IPO the notion of “caveat emptor”, or buyer beware is paramount. While an initial public offering may superficially look just like any other trade one might execute on an exchange, it is a decidedly different beast. Unlike other trades where existing public shareholders sell their shares in exchange for money from a new buyer, an IPO is either a treasury or a secondary offering. In a treasury offering, typically the company is raising money to fund growth plans and the new investor buys shares directly from the company. With a secondary offering, the company does not raise any money, but lists its shares on an exchange and the new investor buys shares from an existing shareholder - quite often the founders of the company, or occasionally from earlier stage investors like private equity or venture capital firms. In both cases, the company’s executive team and board of directors will have hired one or more investment banks to manage the IPO. The investment bankers, for a fee ranging between 3-6% of the value of the deal, advise the company about how to price, structure and market the offering and help create demand for the shares. Understanding the incentives at work here is important: in both a treasury offering and a secondary offering, the selling shareholder’s gain is the buying shareholder’s loss….it is a zero sum game. Treasury shares sold at higher prices raise more money and relinquish less voting control than shares sold lower. Secondary issues sold higher enrich the founders more so and give up less voting control than shares sold lower. Selling shareholders will always prefer a higher valuation and a higher IPO price for this very reason. Investment banks also compete aggressively amongst themselves to win an IPO mandate, since the fees can be very lucrative for a large IPO. Often, the winning investment bank is the one whose pitch to the company’s board makes the most aggressive valuation case for the shares to be issued. Systematic over-pricing of IPOs is the norm in light of these direct and large incentives.

A further peril to an IPO investor is the risk of information asymmetry: the risk of dealing with a counterparty who is better informed about the value of the asset than the buyer. Anyone who has ever bought a used car will understand this…the seller knows intimately how the car was driven and maintained, how often the oil was changed, etc. The casual car buyer kicks the tires and maybe hires a mechanic to give the car a cursory inspection, but nevertheless won’t even approach the deep understanding of the car’s value and condition that the seller has. This is precisely the situation facing an IPO investor. The founding shareholders will have toiled inside their company daily over decades perhaps, accumulating an incredible body of knowledge that an outsider, even a professional investor could never fully replicate. They know their competitive position in the industry, they know customer demand drivers, they understand macro-economic sensitivities in the business, regulatory risks, emerging disruptive competitive forces, supply chain dynamics and a plethora of other value relevant information. Taking the other side of this trade (especially in the case of a secondary offering), and buying the stock at the very time they have chosen to sell is a bold move indeed. The question IPO investors ought to ask themselves is: “if the expert insiders think NOW is such an opportune time to sell, what is it that I know that they don’t that makes me so confident NOW is an opportune time to buy?”

Once issued, a new IPO undergoes a seasoning period in the public markets. This is a multi-quarter time frame where price discovery occurs under less contrived conditions compared with the IPO process. During this time, brokerage analysts initiate research on the stock and publish target prices, which usually validate the IPO price and suggest further opportunity for gains in the stock. Investors should be wary about the objectivity in these reports though, as many of them will be published by the same investment banks who managed the IPO, who will accordingly be extremely reticent to cast their big fee paying corporate client in a negative light with a downbeat initial research report. Establishing management credibility in setting and achieving various operating and financial goals is another important part of the seasoning period. All too often during the IPO process overzealous management teams set very lofty goals for the company, which they are then unable to achieve. In one notable IPO early this year the management team laid out plans to open more than 550 new retail locations over the next three years, with 150-160 new sites in 2017 alone. However, the company had managed to open just 275 stores cumulatively since its inception in 2005. It had taken fully ten years to open their first 178 stores. Not surprisingly, reality set in, and the company was later forced to talk down these hyperbolic hopes and dreams and sure enough, this has been one of the worst IPOs of the year, with the stock down 49%. Nothing irritates a new shareholder more than a company overpromising and under-delivering. Neophyte executives at public companies often don’t foresee the severity of investors’ reaction should they disappoint on key performance metrics. A final argument for allowing a reasonable seasoning period for a new issue is the expiry of management and selling shareholder lock-up agreements. Selling shareholders and key executives typically covenant not to sell any further shares for a certain period of time - usually 3, 6 or 12 months after an IPO. In principle this shows good faith, as new investors don’t want to see a mass exodus of money (and with it, confidence) immediately after they’ve just bought the stock. In practice though, the whole market knows exactly when the lock-ups expire and this can create an overhang on the stock, as investors fear that insiders may dump the shares in droves upon the expiry of the lockup.

The final caution in buying an IPO is the most insidious one: adverse selection, whereby a retail investor will get as many shares of a lousy company as they request on its IPO, but very few or none at all in a good IPO. This isn’t supposed to happen, but it does. Investment bankers managing the IPO are supposed to treat all investors fairly. In practice however, the little old lady in Lethbridge with the $120,000 discount brokerage account buying 100 shares is totally overmatched by powerful pension funds, mutual funds and hedge funds who may not be shy about throwing their weight around and advocating for more than their fair share of “hot IPOs”, knowing that they pay the investment banks millions of dollars in commissions every year, thus crowding out smaller investors on oversubscribed new issues. Related to this notion of adverse selection is the trend of large institutions increasing their allocations to venture capital and private equity, significantly deepening these pools of capital and allowing them to cherry-pick the best opportunities pre-IPO. At the same time, the costs and regulatory burdens associated with a public listing have risen exponentially in recent years, making private financing rounds increasingly appealing for many successful and growing companies that in earlier times might have been good IPO opportunities.

While this missive might sound sombre, or even jaded, we believe that success in investing hinges just as much on avoiding loss as it does on picking winning investments. We won’t poison the well so far as to say that all IPOs should be shunned, but certainly they do deserve a healthy dose of skepticism because the deck of cards is heavily and systematically stacked against new buyers…despite the selective memories of those who spin tales of tantalizingly big wins on new issues. The silver lining in all of this is the fact that systematic mispricing of IPO’s often sets new issues up for a big swoon in their debut year, affording patient investors the opportunity to make their own “initial investment” at a more favourable price and time - as we have done with companies like Shopify, Facebook, Alphabet and Visa, among others from time to time.

Back