After a strong start to the third quarter, financial markets wilted in the final couple of months. Paradoxically, the reason rests largely with the strength and resilience of North American economies, leading to the adoption of a “higher for longer” stance as it pertains to interest rates. The rapid rise of bond yields in August and September scared off bullish equity investors and the bears took firm hold. That said, it’s counter intuitive to be deeply concerned about a stronger economy than had been expected, but this is one of those times when “good news is bad news”. We expect that as the equity market digests the new reality it will realize that an economy can live with mid-single digit interest rates, as evidenced by decades of experience in the modern era.

The Canadian equity market retreated by 2.2% during Q3. Except for the Energy sector (up 8.5%), weakness was pervasive, led by Communication Services (down 12.5%), and Utilities and Real Estate, which both lost roughly 10%.

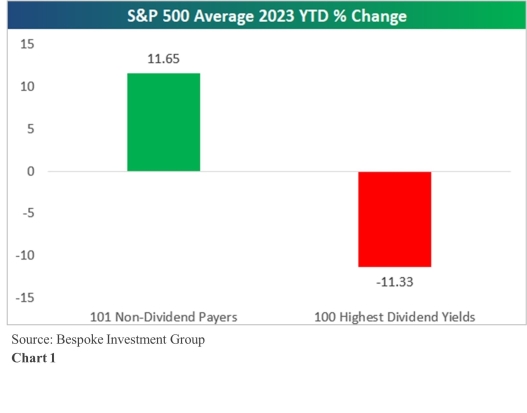

The U.S. based S&P 500 Composite Index lost 3.3% (in U.S. dollar terms) for the quarter, led again unsurprisingly, by interest sensitive sectors, such as Utilities (down 10%), and Real Estate (down 9.7%). Of note, the Consumer Staples sector, which is made up of many well-known branded companies, was down 6.6% in the third quarter. Goodreid has long argued that many of these companies traded at excessive valuations because they had a defensive profile and attracted investors via a relatively high dividend yield. Don’t get us wrong, we love strong dividends, but they should be “right sized” in terms of payout ratio, be attached to growing, quality companies with robust profitability metrics, and have a price valued in a way that can be defended against the market and their own history. As interest rates have risen dramatically the lure of dividends has been dampened by competition from bonds. Chart 1 illustrates that unless an investor is careful, the benefit one receives from a high dividend can be wiped out by a loss of capital. On the positive side of the ledger, Energy stood out as the leading sector, up 11.3% on the back of a 28% advance in the underlying commodity.

The small company Russell 2000 Index was down 5.2% in U.S. dollar terms. Again, rapidly rising rates are threatening to smaller companies who as a group have a more susceptible balance sheet and less access to the capital markets as a funding mechanism. The weaker Canadian dollar during the quarter was a friend to investors with U.S. assets to the tune of about 2%.

The FTSE Canada Short Term Overall Bond Index was unchanged in Q3, demonstrating the relative safety of shorter-term debt instruments. That said, in Balanced mandates Goodreid modestly extended term by rolling maturing issues into 3-to-5-year investment grade corporate bonds. Finally, the Solactive Laddered Canadian Preferred Share Index fell by 2.8% in Q3/23.

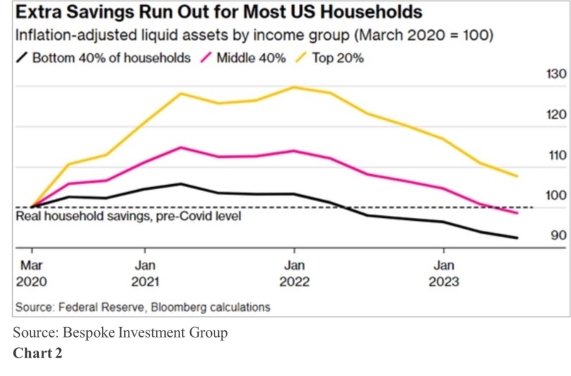

Although North American economies continue to hold up well in the face of higher interest rates, the consumer seems to be running out of steam. The massive stimulus provided during and immediately after the pandemic has carried individuals since early 2020 but as can be seen on Chart 2, most U.S households have now dipped below the savings rate at the time the pandemic hit. This is true for Canadian households as well. Goodreid believes both economies are trending toward a slowdown, and possibly a recession. The good news is that not all recessions are alike.

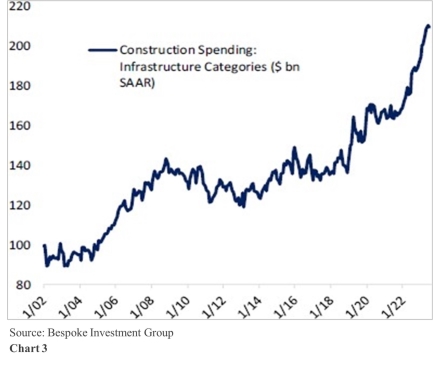

Other parts of the economy are in better shape. The trillions of dollars fiscal authorities have earmarked for infrastructure, computer chip development and inflation reduction efforts have largely yet to be spent. As Chart 3 illustrates, U.S. construction spending has spiked recently, and it’s just the beginning. So, while an economic slowdown is our likely path, it will be felt most on Main Street and affect financial markets to a lesser degree.

Although U.S. corporate profits are estimated to be flat year-over-year in the third quarter, they are trending higher, as can be seen on Chart 4 on the next page. Earnings estimates for the final quarter of 2023 are predicted to advance by 7.8% compared to last year, and for calendar 2024 to grow by 12.2% vs. 2023. Valuations are running at historical norms in the U.S. and are at a discount in Canada. No doubt that is not the backdrop of a traditional recession and is exactly the reason Goodreid thinks this economic slowdown will be unique. Our positioning in cyclicals, industrials, financials and select consumer issues give us confidence in a positive and additive result. Unlike periods in the past when passive investing (i.e., just being in the market) yielded good results, our opinion is that this will be a stock-pickers market, something we do well.

An obvious Canadian market challenge is that the consumer is exposed to housing prices that, unlike the U.S. experience, have yet to see a reckoning, combined with a mortgage rate environment that is much more variable than that in the United States. This is offset somewhat by more modest valuations. In addition, our banking system is concentrated, strong and very well capitalized.

Fixed income is back as a competitive asset class and after being missing in action for many years, now adds value to our return expectations. The playbook for interest rates depends largely on two issues: inflation and the health of the economy. The two are of course related. If higher inflationary trends are persistent, rates will go higher, and the likelihood of a weaker economy grows. A weak economy means central bankers are more inclined to use a reduction in rates to blunt the damage to the economy.

We are comfortable with the composition of our portfolios. On a consolidated basis they demonstrate superior profitability metrics, are growing strongly, and trade at significant discounts to the valuations of their benchmark indexes. That said, we are continually monitoring the companies we own on our clients’ behalf and will make necessary changes.