The defining event for financial markets in the first quarter of 2023 was, without doubt, the failure of a couple of U.S. regional banks and the resulting fear of contagion. After a few weeks of financial angst, the dust seems to have settled, but not without some likely lasting effects on the financial system and world economies. The core cause of this “financial accident” was the rapid, and some would say, heavy-handed, action of central bankers who have increased interest rates in a very aggressive manner over a short time period. In this environment, one bank in particular, Silicon Valley Bank, mis-managed their risk exposure, ultimately leading to a classic “run on the bank” by depositors. However, in 2023, a run on a bank is much different than it was a century ago, during the Great Depression. Digital access to deposits proved troublesome, exacerbating the psychological group-think aspect of the phenomenon. The scarring effect of the banking failures will likely lead to greater regulation (regardless of whether regulation was the issue), and certainly lead to greater caution by banks in the form of tighter lending standards. The result will be a slowing of economic growth, but as a positive effect, a damping of inflationary pressures.

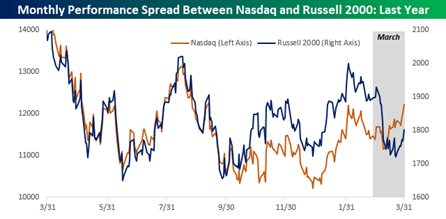

The banking failures overwhelmed other important influences on the financial markets as well as causing a ripple effect on related asset classes. Inflation is waning, but to some extent has been pushed off the front pages by the banking issues. Paradoxically, the bank issues may save the Fed from digging an even deeper hole by creating a pause in their tightening program. Most notable among the ancillary effects of the regional bank worries was a strong rally in the bond market as interest rates fell sharply in anticipation of the Federal Reserve and other world central bankers taking a break in raising rates, as well as an increased probability of a recession. The trickle-down effect on equity markets was a surge in growth stocks, notably technology shares, which tend to rally on lower rates. Banking shares were predictably weak. Chart 1 illustrates the strong rally in the tech-heavy Nasdaq Index (up 9.5% in March), at the expense of the small company Russell 2000 index (down 4.9% in the same period).

The Canadian equity market gained 4.6% during Q1 and was not seriously affected by the dislocations of the U.S. banking sector. One must recognize that while Canada and the United States share many similarities there are also marked distinctions, including the structure and composition of our banking sectors. There are over 5000 banks in the U.S., many closely owned and controlled, with a variety risk profiles, while Canada has only 35 domestic chartered institutions, all highly regulated.

The U.S. based S&P 500 Composite Index fared better, gaining 7.4% for the quarter, but it is worth noting that the large tech components of the index drove much of the gain. The equal-weighted S&P 500 Index advanced only 3%. The month of March showcased wild divergences. Highlighting some details depicted within Chart 1, the U.S. Financial sector was down 9.5% in the month, while Technology was up 10.9%. As our friends at Bespoke Investment Group noted at the end of the quarter, “It was a quarter where more risky stocks with higher P/E ratios, higher price to sales ratios, and higher short interest levels outperformed by a significant margin as well. The 50 stocks with the highest P/E ratios at the start of the year gained 13% in Q1, while the 50 stocks with the lowest P/E ratios fell 2.5%.”

The small company Russell 2000 Index gained 2.7% in U.S. dollar terms. The relationship between the U.S. and Canadian dollar was largely unchanged, so foreign exchange had little effect on returns. The FTSE Canada Short Term Overall Bond Index advanced 1.8% in Q1. Finally, the Solactive Laddered Canadian Preferred Share Index fell by a fraction in Q1/23.

So, all in all, balanced accounts fared reasonably well, but under the surface there were big winners and losers. Much of the action seemed of the “knee-jerk” variety, as evidenced by the fact that the top decile performers in Q1 were the bottom decile performing group for all of 2022. Having experienced this type of event-driven divergence in the past, we would caution against a presumption that we will witness more of the same. Odds are there will be an unwinding of the extremes.

Goodreid’s Canadian equity portfolio had a strong start to the year, outperforming the S&P/TSX Index smartly. Our outperformance was led by individual stock selection which saw four standout companies in three different sectors. While every sector within our Canadian equity portfolio finished the quarter in positive territory, Technology, Consumer Discretionary, and Consumer Staples were stellar performers, with returns of 25%, 12% and 11%, respectively. The four key companies that drove Goodreid’s Q1 performance were found within these sectors, namely: Topicus (+35.9%) a European-based software company; Canadian Tire (+26.0%) a diversified retailer; Constellation Software (+22.7%) a large software concern; and Alimentation Couche-Tard (+14.5%) a convenience store operator.

Three of these four companies are recent additions to the Goodreid Canadian Equity portfolio, illustrating the success of our revitalized investment strategy in the Canadian equity portfolios. Our revitalized strategy focuses on owning high quality companies purchased at attractive valuation multiples.

The weakest performance came from the Energy sector, which still finished the quarter in positive territory, up 0.5%. Tourmaline Oil (-14.7%) was the worst performing company as prices for natural gas remained weak, down 51% in the quarter.

In the quarter, we opportunistically added new positions in BCE and TC Energy. Also, as banks experienced weakness due to the Silicon Valley Bank (SVB) failure in the United States, we took this opportunity to increase our bank weight in Canada, adding shares in TD Bank. In the first quarter we also received shares in Lumine. Lumine became a separate public company following a spin-off from Constellation Software, which is already owned in the portfolio.

Weights in Saputo, Canada’s largest dairy manufacturer, and Stella Jones, a railway tie and utility pole manufacturer were reduced, harvesting profits, and redeploying those proceeds into other investment ideas.

The U.S. portfolio performance statistics in Q1, 2023 were mixed. The large capitalization portfolio underperformed the S&P 500 index given the outsized effect of a few mega cap names within the cap-weighted index. When compared to the performance of the S&P 500 Index on an equal weight basis, Goodreid’s large cap U.S. portfolio performance was in line. Conversely, our small cap portfolio outperformed its benchmark, the Russell 2000, by a wide margin in the quarter, largely due to the strong performance of the Homebuilding sector and our under-weighting of U.S. regional banks.

On a sector and name basis, Technology and Communication Services companies held in the large cap portfolio, not surprisingly, were strong performers, up an average of 19%. Leading the way were Bookings Holdings (up 32%), and Apple (up 27%). Detractors for the quarter were Healthcare holdings, CVS (down 20%) and Elevance (off 10%). Our Financial holdings were surprisingly strong, as large banking institutions were the beneficiaries at the expense of smaller banks. J.P. Morgan (JPM), for example, fell only 3% in the quarter.

Activity within the U.S. large cap portfolio was robust in the quarter. Entering the portfolio early in the quarter were shares in Adobe (ADBE), Amgen (AMGN), Chevron (CVX), Deere (DE), all high-quality companies, with identifiable catalysts for growth, trading at attractive valuations. We exited Fedex (FDX) on execution fears and reduced confidence in management, and Honeywell (HON), on valuation. Late in the quarter we took some profits in Booking Holdings (BKNG) and added to our positions in Amgen (AMGN), and Visa (V).

The U.S. small cap portfolio benefitted from exposure to Homebuilders and Industrials. Goodreid owns five homebuilding stocks in the Small Cap portfolio, which have served clients very well. We believe homebuilders have the fundamental strength and positioning to take advantage of the decades-long underinvestment in new housing. In Q1 the five combined issues were up an average of 23% yet continue to represent outstanding quality and value. Industrials, such as Clean Harbors (CLH), O-I Glass Inc. (OI), and Regal Rexnord (RRX), advanced sharply. On the downside were the aforementioned regional banks, the troublesome ones in the portfolio being PacWest (PACW), Bank United (BKU), and Synovus (SNV). While they fell sharply in the quarter, we believe they are sound financial institutions. That said, the unknown of possible contagion leads us to take a cautious stance and stand pat with our holdings. Smaller financial institutions, unlike their larger competitors, have a higher degree of company-specific risk.

In conclusion, it was an interesting and active start to 2023. Our expectations, as outlined in past quarterly commentaries, of this year defining the end of this bear market remain intact. That said, volatility often accompanies a transition to a new growth phase, and we are positioned and prepared for that. Regardless of the macro-economic environment, you can count on Goodreid to stay focused on identifying and managing high quality companies, purchased at attractive valuation multiples.