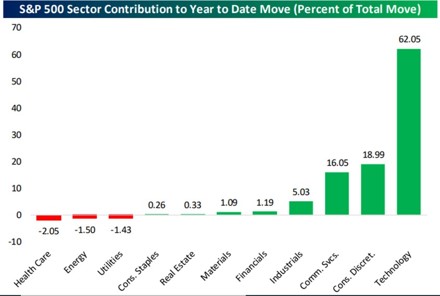

As much as regional financial stocks dominated the narrative in Q1, the market talk in Q2 was Artificial Intelligence (AI). Other issues, although continuing in relevance, took a backseat, but at Goodreid we are keeping a keen eye because the path of inflation, interest rate hikes, the health of the Canadian and U.S. economies, not to mention the Chinese economy, are likely to play more into future market opportunities than AI. As can be seen on Chart 1, the Technology sector contributed the majority of the year-to-date return for the U.S. based S&P 500 Index, and when you add Communication Services (which includes the likes of Apple, Meta, Amazon and Microsoft), nearly 80% of the year-to-date return can be accounted for.

Chart 1

While the AI concept is exciting and full of promise, a review of company price moves reveals that at least some of the future promise has been built in. At Goodreid we feel we have an appropriate exposure to AI through ownership in companies like Amazon, Alphabet (Google), and Adobe. A review of lagging sectors is interesting. The left side of Chart 1 highlights the underperforming or dormant sectors, which are becoming less and less expensive as their fundamentals improve yet their stock prices languish. Chart 2 illustrates this, as Healthcare and Energy stand out as being historically inexpensive.

Chart 2

In Canada, known for its commodity-centric economy, the prices of energy related companies were relatively flat. Our representation in this sector offers great promise, as production costs have been driven lower through both technology and prudent management. Sooner or later, the sector will “catch a bid”, but energy prices worldwide are being affected more by supply issues than demand. Over time, a more attractive balance will be struck as the appetite for investment wavers. Other areas of our economy offer promise and we are pleased to own positions in industrials, consumer companies and technology concerns that continue to contribute.

The Canadian equity market gained 1.1% during Q2, led by Information Technology (+16.6%), Consumer Discretionary (+6.4%), and Industrials (+2.1%). The major detractor was the Materials sector (-6.9%). The banking group (which turned in a fairly neutral performance in Q2 appears to be digesting higher interest rates and the nagging concerns that their mortgage loans could be problematic. Given recent events in the U.S. banking sector, we were encouraged to hear that deposit growth trends amongst Canadian banks had not been disrupted. Commentary was consistent across the group, for both the Big Six banks and some of the smaller banks as well. Separately, Bank of Nova Scotia, which Goodreid holds in our Canadian Equity model, indicated that the deposit business in its Latin American footprint was exhibiting similar stability to what it was seeing in Canada.

With respect to the Big Six banks’ mortgage business, banks are not seeing friction in terms of delinquencies as borrowers seem to be absorbing increases in interest rates. They quantified that borrowers renewing mortgages were seeing their monthly payments increase by

$200 - $600. Also, refinancing activity, which allows borrowers to extend amortization in order to reduce payments, was at normal levels. Customers appear to have cash flows currently to absorb the higher payments, due to higher salaries and savings.

The U.S. based S&P 500 Index fared better than its Canadian counterpart, gaining 8.7% for the quarter, but the large tech components of the index drove much of the gain. The equal-weighted S&P 500 Index again trailed, advancing only 4% in the quarter. Chart 3 tracks the relative strength of large and small companies. Note that the recent outperformance of U.S. large cap companies follows an abysmal performance in 2022. We wrote an article that can be found on our website (sign in/up through Articles section), entitled U.S. Market Bifurcation: The Story of Two Markets, that explores our theory on the rapid rise of large growth stocks since early March, coincidental with the beginning of the regional banking crisis in the U.S. We encourage you to access this article to understand our thinking more fully with regard to this market phenomenon.

Chart 3

The small company Russell 2000 Index gained 5.2% in U.S. dollar terms and 3% after the Canadian dollar translation, the result of a strengthening of the Canadian dollar during the quarter by about 2%. The FTSE Canada Short Term Overall bond index lost 0.8% in Q2, as short-term rates powered higher. After years of earning meager returns within the Fixed income market, bonds are now presenting viable competition with other asset classes and are a complementary component to a portfolio. In the quarter, we extended bond terms to capture attractive rates. Finally, the Solactive Laddered Canadian Preferred Share Index fell by 1% in Q2.

After such a strong start to 2023, one can expect occasional bull market corrections. History books will define the current bull market in the U.S. from the low market levels of last October. To date, the U.S. large cap market has advanced during this “bull” cycle by 24% and the U.S. small cap market by 14%. Canadian markets have been more stable since the pandemic, avoiding the textbook definition of a “bear” market since the post-Covid rally of 2020.

Chart 4 is a sentiment tracker as defined by the American Institute of individual Investors (AAII). It tends to negatively correlate with market direction and is now at the highest recording since early 2022. Over the past weeks and months, a building feeling amongst investors of FOMO (fear of missing out) has been evident. A natural cooling of equity markets would be both normal and healthy, but likely also modest in duration and severity.

Chart 4

On balance, it was a constructive quarter for North American financial markets. Within the Goodreid equity portfolios, winners outpaced losers to allow us to add value to your portfolio, both in absolute terms and when compared to appropriate benchmarks. As always, regardless of the macroeconomic environment, you can count on Goodreid to stay focused on identifying and managing high quality companies, purchased at attractive valuation multiples. As well, fixed income investments have again become relevant again, and we are slowly extending term to capture opportunity, a welcome relief after years of near-zero rates offering no investment value.