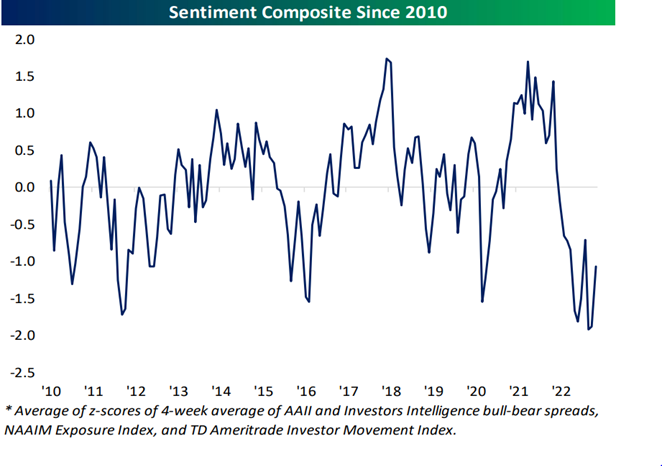

The year 2022 will, without doubt, go down as a difficult year on many fronts, including investors’ experiences. At Goodreid, we are thankful for our clients’ patience as we navigated a changing economic, political and health landscape. Investors were steadfast in their negativity; in fact, not one week in the entire year recorded positive investment sentiment trumping negative sentiment. The below chart illustrates that investors were in a bad mood. Looking back a dozen years in the post-2008 period, 2022 witnessed the poorest sentiment. We are encouraged that, historically, this has been a positive market signal, yet another life example illustrating that “the crowd” is usually wrong.

The fourth quarter provided some relief to an otherwise poor year for North American equities and fixed income. At Goodreid, we exit 2022 with mixed feelings. On one hand, we are disappointed not to have grown our balanced investment accounts as we have in most of the prior years, but in another way, very satisfied to have limited the damage in a very challenging environment by soundly outperforming benchmark indexes and competitive managers.

The Canadian equity market gained 6% during Q4, leading to a yearly tally of negative 5.8%. The U.S. based S&P 500 Composite Index fared considerably worse, off 18.1% in local currency for the year after a positive Q4 return of 7.6%. When translated to Canadian dollar terms, Q4 returned 6.1% and the yearly tally was negative 12.2%. The small company Russell 2000 Index fell by 20.4% in U.S. dollar terms for the year (plus 6.2% in Q4). The FTSE Canada Short Term Overall Bond Index advanced 0.7% in Q4 but was down 4.1% for the year. The Solactive Laddered Canadian Preferred Share Index performance rounded out a dismal year by falling 3.3% in Q4 and retreated 17.2% for all of 2022.

We are pleased to report that Goodreid’s Canadian equity portfolio rose in 2022, and both the Goodreid U.S. large and small capitalization portfolios outperformed their respective benchmarks by a meaningful margin, the result of active management techniques and strong stock selection.

Our positioning in 2022 served clients well. In the Canadian portfolio, we focused on the following:

ALTERED the Sector weightings in our portfolio

INCREASED the Quality of holdings in our portfolio

INCREASED the Number of holdings in our portfolio

SHIFTED into Value

The U.S. markets faced a more difficult backdrop than those in Canada because of a higher concentration of Technology and Communication Services stocks vs. the dominance within the Canadian markets of one of the few sectors that worked for most of 2022 – Oil & Gas. We actively managed our U.S. exposure in 2022, selling our META (Facebook) position completely and significantly trimming our exposure to APPLE. The US large cap portfolio also expanded its number of holdings and created an overweight position in defensive sectors such as Healthcare.

When viewing the consolidated holdings within our two U.S. portfolios – the Large Capitalization and the Small Capitalization – we gain comfort. The Large cap portfolio trades at a reasonable 13.7 times trailing earnings, is expected to grow earnings at a 13% plus clip in 2023 and has a 20% return on equity. The Small cap portfolio should also fare well. At less than 10 times trailing earnings, it has good growth prospects and strong stability and risk characteristics.

The Fixed Income market in 2022 did not provide a hedge to a negative equity market that it often has in the past. In fact, as interest rates rose relentlessly in 2022, holders of bonds, especially those with maturities well out in the future, were financially hurt. Goodreid’s strategy of holding predominantly short-term bonds continued to benefit our clients. As we ended 2022, based on our belief that the bulk of interest rate increases are in the past, our strategy evolved into a more neutral stance on Fixed Income, by extending term and using bonds as a constructive source of income for portfolios.

While we write to you each quarter outlining our thoughts, year-end commentaries often take on a different hue, looking back a little further and reflecting on what may lie ahead. As we stated earlier, investors world-wide were bloodied in 2022, the result of central bankers raising interest rates in an effort to tame inflation. This medicine kills the disease (inflation), but also can severely weaken the patient (economies and stock markets). The good news is that the patient always recovers. The bad news is that a recession is often a byproduct of achieving the desired result. Inflation is rolling over and almost certainly will continue to fall. However, central bankers have specific inflation targets, and it is likely that accelerated job losses and muted wage growth will be required to achieve those targets.

So, given all that, what can we expect of equity markets in 2023? We are cautious, but optimistic. Here are seven reasons why:

Chart 2:

Chart 3:

Of course, just because the calendar turns doesn’t mean the “all clear” will be sounded. We expect the process to unfold, with inevitable bumps in the road. One thing is clear to us, in 2022 the medicine was administered, and we expect 2023 will be a recovery year.

While our view of financial markets is that 2023 has promise, we continue to be cautious. Transition years can be volatile and as we move through the rough waters of recession and tepid earnings results, the markets will be cranky for periods of time. Goodreid’s active management will attempt to curb the effects of down periods and take advantage of the inevitable recovery. Adding value, regardless of the environment, is a sound objective, if you believe as Goodreid does, that over the long-term capital-based economies will grow and that well-positioned companies within the economies will achieve superior results.

We wish everyone a healthy, happy, and prosperous New Year.