Presidential Cycles & Markets

Goodreid eArticle, Fall 2022

View As PDF

The 2022 midterms took place on November 8, and there is no shortage of news commentary about winners, losers, and what is shaping the political cycle. There is a famous saying – history doesn’t necessarily repeat itself, but it sure does tend to rhyme. This year is no exception, and with Republicans set to take over the House, with the Democrats controlling the Presidency and Senate, we are looking at 2 years of a split government until the next Presidential cycle begins.

Is this a good thing? How are markets going to behave? Will there be more upside or downside in an environment with high inflation and a likely (if not current) recession? A look into what has happened in the past may give us some clues about what is going to happen in the future.

How Have Markets Performed Before and After Midterm Elections?

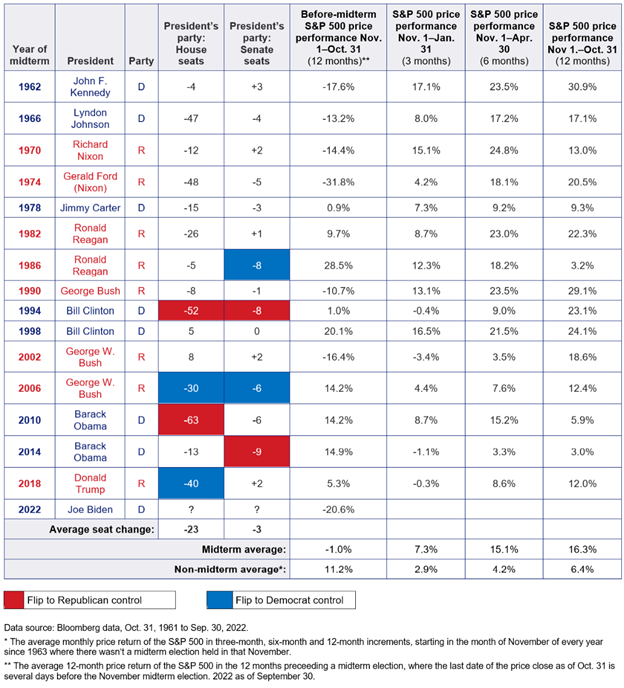

One thing we should preface before going any further is that, of course, every election cycle is different, and no prior period can predict a future outcome. However, taking a look at the empirical evidence can give us some solace into what has been a truly challenging stock market in 2022. Going back to the 1962 midterm election cycle, we can see in the table be-low that the 12 months leading into midterm elections has been negative on average, with an overall return of -1% (some years much worse than others):

Source: US Bank

And, of course, 2022 has been one of those negative years with a return of -20.6% leading up to the midterm election cycle.

What has historically happened in the 3, 6, and 12-month period after midterms is, truly, eye-opening. Despite changing power structures, split House and Senate chambers, and wars, among other things, one thing has remained remarkably consistent – positive stock markets. While there are some negative 3-month periods post midterm elections, the average first quarter return is 7.3% for the S&P 500 Index following elections. And the 6 and 12-month returns are even more no-table – every single one has a positive return, with averages of 15.1% returns for the 6-month period and 16.3% for the 12-month period. In all three forward time periods, there is an highly differentiated outperformance from all years where there isn’t a midterm election, and a pronounced underperformance in the 12-months leading up to a midterm election cycle.

Let that sink in for a minute or two. We’ve just experienced one of the worst 12-month periods leading up to midterm elections, second only to 1974. And in every single one of those cycles, markets have been decisively positive in the 6 and 12-month periods following it.

2 years in, 2 years to go

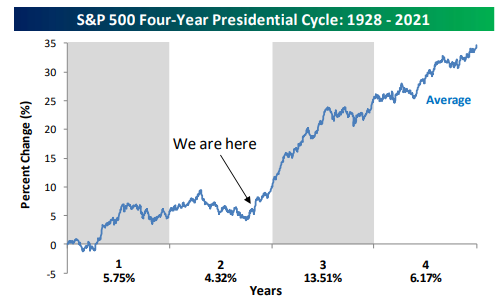

Now that we’ve gotten past the midterms, the next major election cycle is going to be Presidential. How time flies. Until then, though, we have two years left of President Joe Biden’s White House. Historically, since 1928, the first two years of a presidential cycle have been muted, with average annual returns of 5.75% and 4.32%. However, when you look at years three and four, things start to get exciting.

Source: Bespoke Research Group

Year three of each presidential cycle going back to 1928 has returned an average of 13.51%. That is something to take note of. And year four comes in at respectable 6.17% average.

Does this mean, entering year three of the current presidential cycle, we’re going to get a double-digit return? It wouldn’t be shocking, especially after enduring a bear market in 2022.

Sentiment Remains Negative

In addition to the presidential cycles, it is important to look at the current state of the market, and the headlines surrounding what to expect. Inflation is rampant, although it looks to be possibly peaking or has peaked. Recession indicators are flashing red, with central bankers tightening monetary policy around the world. The once untouchable tech stocks are reeling, with the “everything rally” turning into a “flight to quality”. Bonds have provided no protection in the current market pullback. Safe to say, sentiment around investing in risk assets is negative.

However, positioning too conservatively could be a mistake for investors. Although markets can and may slide further, we have to remember we are well into a bear market.

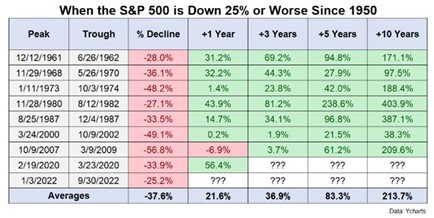

Yes, it’s time to take another look at history. We crossed past the -25% level from the peak of the market back in September this year. There have been eight other times since 1950 that this has happened. After crossing -25%, the 1, 3, 5, and 10-year returns following each of those times is displayed below :

Source: Bespoke Research Group

Not a bad track record. Worth noting, markets can definitely get worse before they get better – but if you maintain your strategy and conviction, long term, you can reap some impressive rewards.

Are we repeating the 1980s?

We reference the late 1970s and 1980s here because of some similar characteristics, especially in regard to inflation. There are some striking similarities, including how the Federal Reserve (Fed) is attempting to cool inflation by raising interest rates significantly, potentially causing a recession. The former chairman of the Fed in those times, Paul Volker, was widely credited with taming inflation by any means necessary – raising rates significantly in a time of uncertainty. He often is credited as a hero of the era, eventually returning the country to a prosperous, low-inflation state.

However, history books tend to forget he did make mistakes in his tenure. Around 1980, Volker relented his hiking phase after a recession damped inflation, but began to cause structural economic issues. This was not the optimal outcome, as in 1981 inflation roared back, and the United States had its worst recession and economic downturn since the Great Depression.

Are we on the same course here, with the Fed under Jerome Powell slowing down interest rate hikes by either too much or too little? We will have to wait and see. One thing we do know, though, is that some short-term pain is far better than long-term dislocations. The cost of not doing enough on interest rate hikes is likely going to be far more than doing too much. As one commentator was quoted as saying, “you’d rather build the bridge 100 feet too long than 10 feet too short”.

The Markets in 2023 and Beyond

Stock markets have a way of humbling investors. Right when you think they are going to recover, they tend to falter, and vice-versa. We have been through an extremely challenging period in 2022, where not much seems to be going right for stocks. Interestingly though, financial pain can also bring opportunity. The correlation of returns with Presidential election cycles, coupled with the historical pattern of market action following a 25% market decline, introduces compelling arguments for adding risk to your portfolio. While there will be bumps in the road and volatility may be heightened, the historical evidence supports an attractive outlook for stocks and other risk assets.

Back